Published on: June 10, 2026

Nexperia Discretes Are Still Stuck: How the Dongguan Export Halt Hits Your Industrial and Automotive BOMs — and What to Pull Now

The Nexperia disruption that started in late September 2025 still isn't resolved. Export out of the Dongguan back-end plant is jammed, and some legacy parts won't see new material until July 2026 or later. This isn't a slow price story you can absorb — it's cheap diodes, MOSFETs, and logic gates that stop a line when a single one goes missing. Here's a working checklist for spot buyers and industrial procurement.

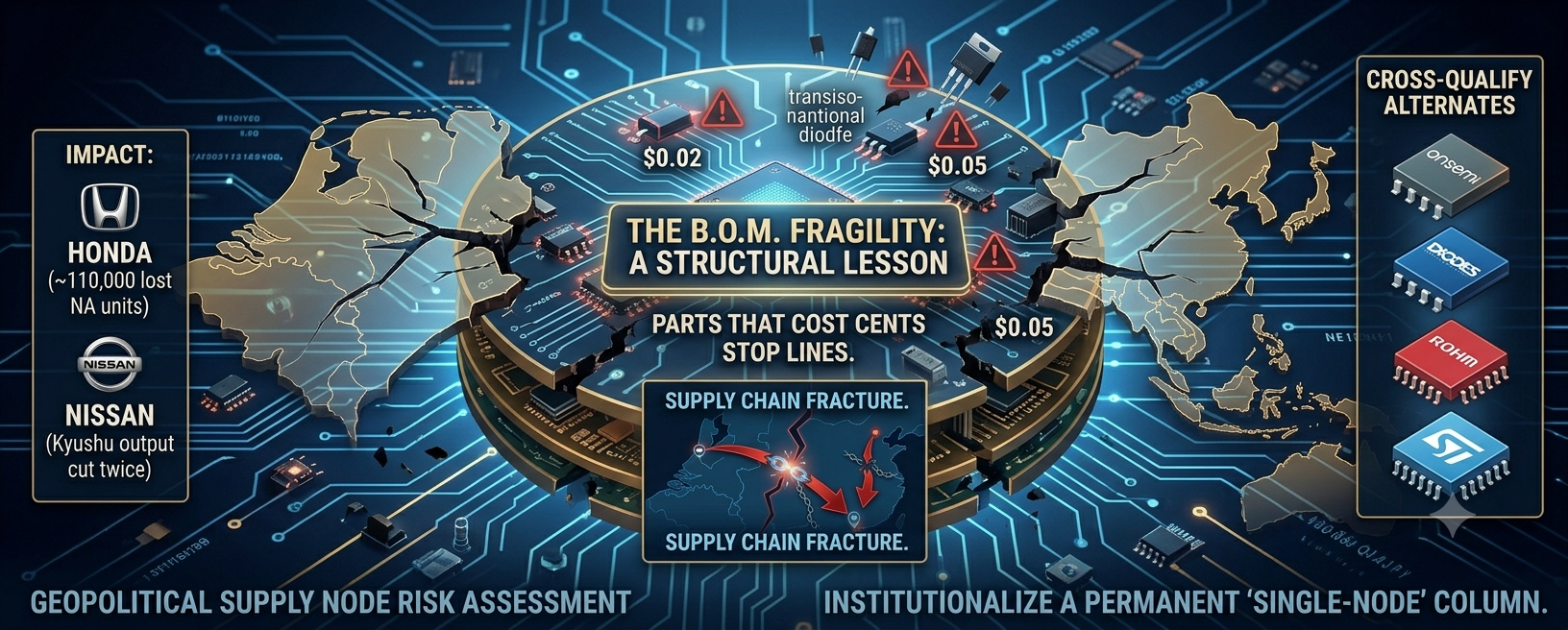

Start with the shape of it. Nexperia runs about US$2 billion in annual revenue, with roughly 60% going into automotive. The bread and butter isn't anything exotic — it's logic gates, small-signal diodes and transistors, ESD protection, and MOSFETs. Parts that cost cents, go onto a board by the dozen or the hundred, and stop the whole line when one is missing. That's exactly where the pain lands: cheap, invisible, and a single-line-down risk.

The mechanics: in late September 2025 the Dutch government took control of Nexperia's Netherlands operations, and Beijing responded by halting exports from the Dongguan assembly-and-test plant. With back-end packaging stuck in China, front-end wafers and final test stopped lining up, and product couldn't ship. Honda flagged roughly 110,000 lost North American units and about ¥150 billion in impact; Nissan cut Kyushu output twice in November 2025. As of June 2026 it still isn't fully cleared — customers on higher-risk legacy parts are being told new material may not arrive until July 2026 or later.

For spot and industrial buyers, the move right now isn't to watch. It's to scrub the BOM.

Go through every BOM and flag every Nexperia reference designator. The ones that matter aren't the high-volume lines — they're the positions that are Nexperia-only, old package, low usage, but a hard stop if pulled. Those are the references that vanish mid-build, and a re-spin won't land in time.

Sort by substitutability into three buckets. Pin-to-pin swaps (equivalent small-signal parts from onsemi, Diodes Inc, Rohm, ST) — open a second source now, get the drawing and AVL updated ahead of the gap, don't wait for the line to drop before you start the change order. Semi-compatible parts that need a board tweak — queue the engineering eval today. Truly sole-source, can't-be-changed parts — run last-time-buy math and cover the lifecycle.

Be careful on the spot market. When parts like these go short, the secondary market lists them within days — but small-signal discretes carry far higher refurb, mixed-lot, and remarking risk than big silicon. A few wrong date codes blended into a reel are something you simply won't test out. Trust the channel, the original packaging, and date-code consistency; small-lot qualify before any large buy. Lock the date code and package before you sign an NCNR.

Don't get optimistic about alternates either. onsemi, Diodes, Rohm — the players absorbing this demand don't have infinite capacity, and as Nexperia's volume lands on them their lead times are stretching too. Speaking up early, ordering early, and locking allocation early beats chasing spot later.

The closing thought is about the logic itself. The root of this shortage isn't insufficient capacity — it's that one process step, assembly and test, sits on a single geopolitically exposed node. Today it's Nexperia. Tomorrow it's someone else. The thing actually worth keeping isn't this one save — it's the discipline of writing "single geopolitical node = single point of failure" into the risk column of every critical BOM, starting now.