July 29, 2026

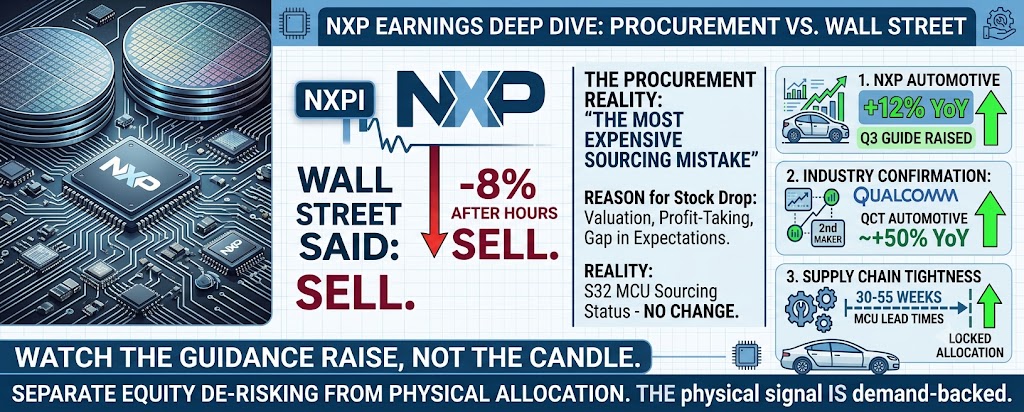

NXP Booked a Record Automotive Quarter and the Stock Still Fell 8% — The Spot-Buyer Read

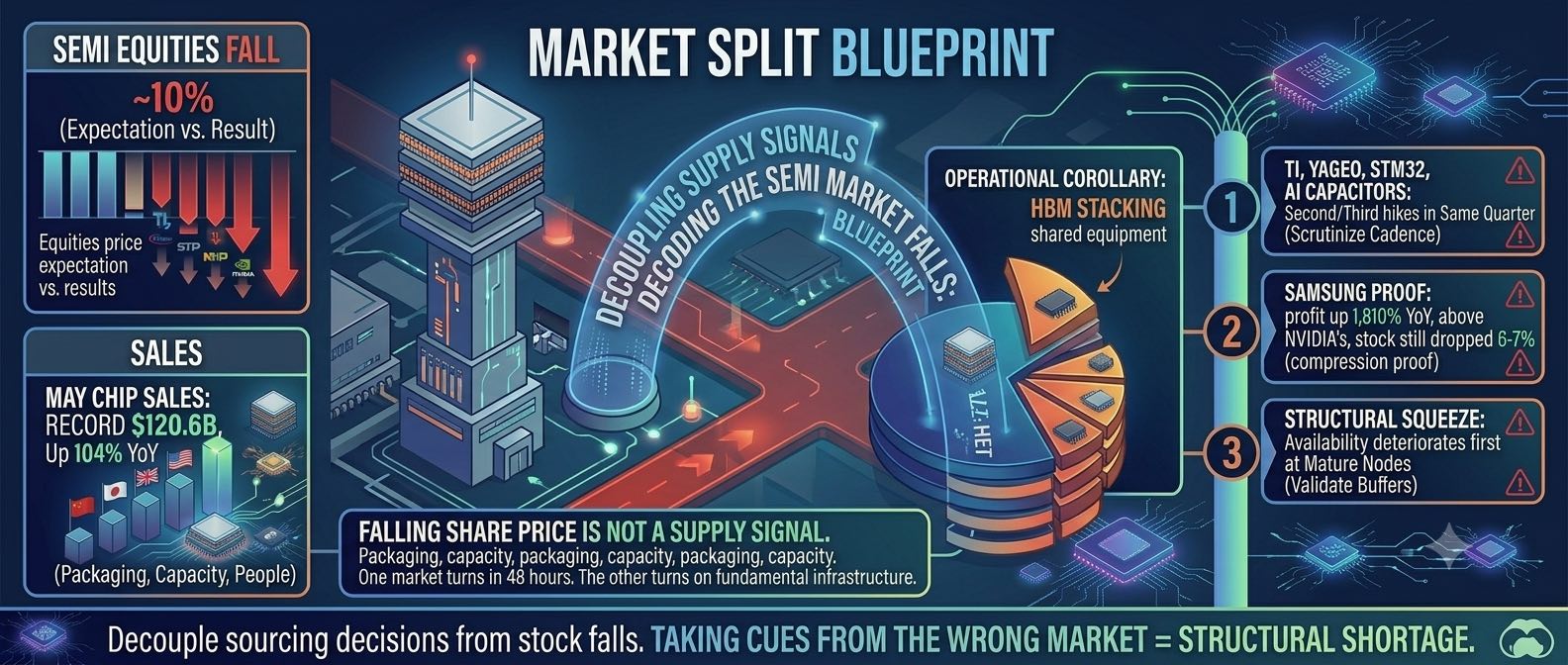

NXP beat on revenue and EPS in Q2 2026, grew automotive +12% YoY (+17% ex-MEMS), and raised Q3 guidance — and the stock still dropped ~7.7% after hours. The real signal isn't 'NXP fell.' It's that financial-market sentiment and physical allocation are running on two separate tracks. Here's how to quote and negotiate automotive parts around that.

marketprocurement2026-q2supply-chain

Read more →