Published on: June 8, 2026

The Helium Squeeze Just Pushed the Shortage Upstream: How One Gas Throttles Memory and EUV Nodes

While everyone watches DDR5 and HBM quotes, the real trigger this week retreated to a single canister of gas. Iran hit Qatar's Ras Laffan, ultra-pure helium spot prices doubled, and Korean fabs started rationing. Here's the helium line in plain terms — who's exposed, which parts it touches, and how spot desks should play it.

Everyone's been staring at DRAM and HBM price sheets, tracking the double-digit jumps. But the thing worth writing down this week is a canister most people never mention — helium.

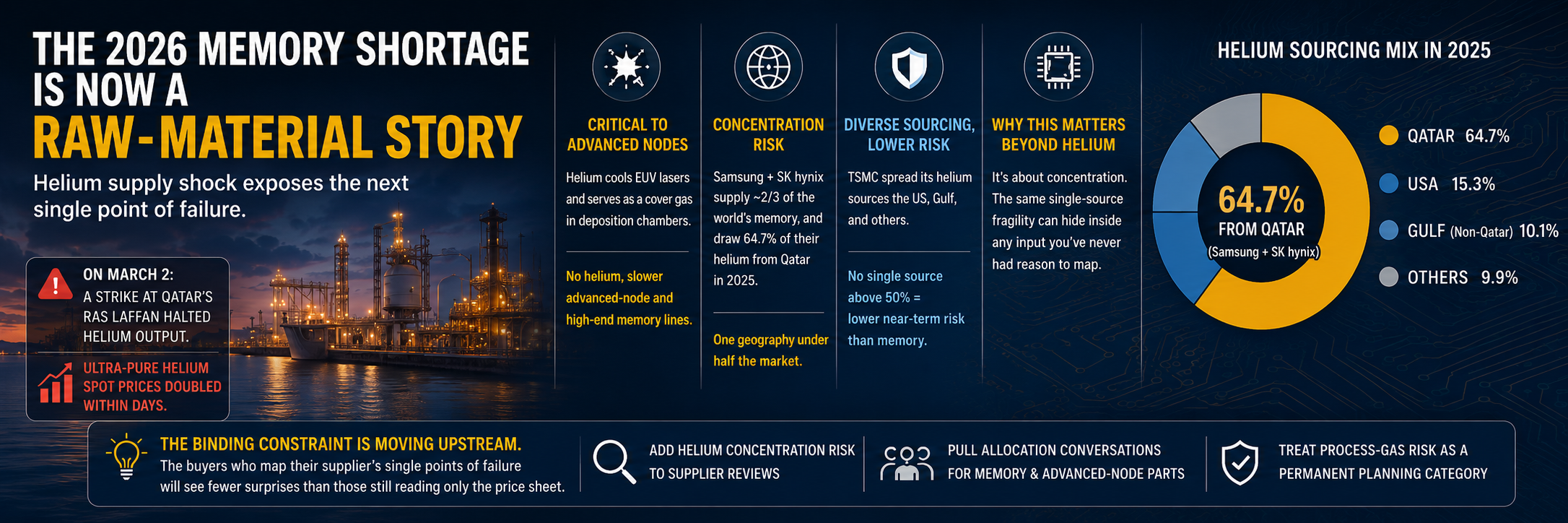

On March 2, Iranian drones struck Qatar's Ras Laffan Industrial City, one of the largest LNG and associated-helium hubs on the planet. QatarEnergy briefly halted all LNG and helium output. Helium shipments through the Strait of Hormuz stalled.

The result was immediate: ultra-pure helium spot prices doubled, and Korean fabs began rationing.

Why does helium matter? It isn't a consumable you can swap out. It cools the lasers in EUV lithography and serves as a cover gas in deposition chambers. Without it, advanced-node and high-end memory lines slow down.

Who's exposed comes down to one number:

- Samsung + SK hynix together supply ~2/3 of the world's memory.

- In 2025, those two drew 64.7% of their helium from Qatar.

- One supply line, half the memory market.

TSMC is relatively insulated. Its helium spreads across the US, Gulf, and other suppliers, with no single source above 50%. That's why, in the same shock, logic faces lower near-term risk than memory.

Translate the line into parts:

- Memory (DRAM, DDR5, enterprise NAND/SSD, HBM): one more upstream uncertainty stacked on an already-tight market.

- EUV advanced nodes: 3nm/2nm cycle times take the hit when helium tightens.

- Downstream PC, mobile, AI servers: cost keeps passing through — PC OEMs are already flagging 15%-20%.

For spot desks and brokers, a few things to do now:

- Treat 'helium-sensitive' as a new part attribute. Push memory and advanced-node parts up your stocking priority.

- Lock allocation and long-term contracts where you can — recovery from a geopolitical event like this is measured in months, not days.

- If you're holding memory-class excess inventory, re-check your pricing window. When the upstream tightens, the spot bargaining position shifts.

- Don't read the June 5 AMD/Intel-led sell-off as fundamentals easing. The tape is sentiment; the supply picture is unchanged.

The trouble with the helium line is that it isn't on most radars. People model wafer capacity, HBM stack height, CoWoS slots. But a single gas can slow an entire memory market.

The logic of this shortage is shifting from 'OEM repricing' to 'raw-material supply shock.' Reading that direction matters more than chasing any one part's quote.