Published on: May 29, 2026

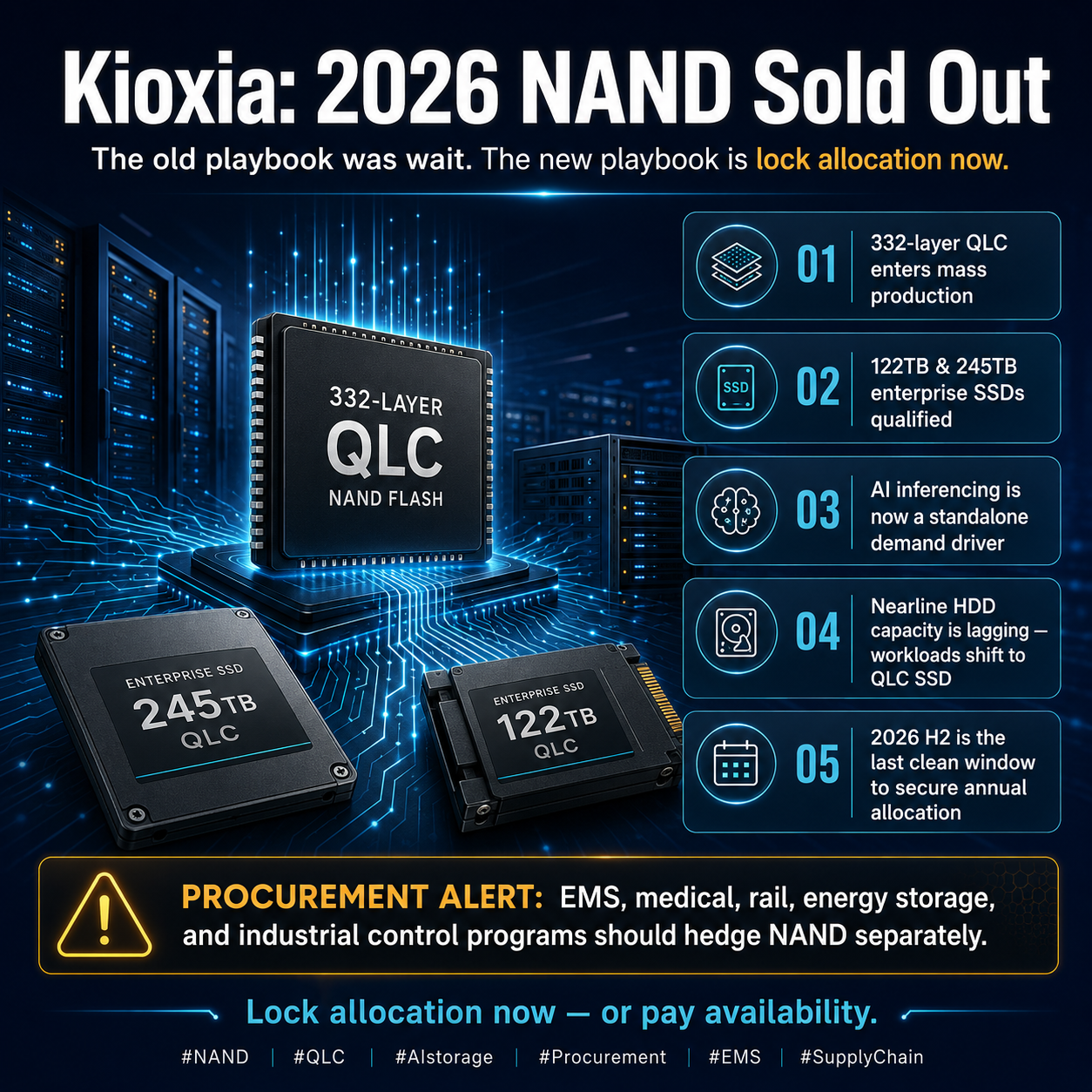

Kioxia Sells Out 2026 NAND While 332-Layer QLC and 122TB / 245TB SSDs Push Nearline HDDs Out of AI Inference Stacks

Kioxia management has stated outright that calendar 2026 NAND production is already sold out, with tightness running into 2027. The 332-layer QLC node is moving into mass production, 122TB and 245TB enterprise SSDs have cleared customer qualification, and AI inferencing plus nearline-HDD displacement are quietly becoming the second leg of NAND demand.

1. What Kioxia actually said

The memory business managing director at Kioxia, in a recent public statement, made it clear: calendar 2026 NAND production is sold out. Delivery dates and quantities can no longer be adjusted on customer demand, and the company is moving to "gentleman's agreement" annual supply plans with strategic partners.

Tightness is expected to run into 2027. Even Kioxia's long-term customers are now absorbing year-on-year price increases of up to 30%.

Translation for the buy side: you no longer book volume against a quarterly forecast. You sign an annual allocation, and if your annual number is wrong, you are paying spot or you are not getting silicon.

2. 332-layer QLC and 122TB / 245TB are not marketing slides

Kioxia has showcased 332-layer process technology. On the product side, 122TB and 245TB QLC enterprise SSDs were shipped for customer qualification at the end of CY2025 and are moving into mass production this fiscal year.

Put the two together. A single drive at 245TB lets a 2U server with 24 bays land at roughly 5PB before any RAID overhead. That is the density AI inference data lakes have been waiting for.

3. The demand mix has shifted

Kioxia spells out three drivers for 2026 NAND demand:

- Traditional server replacement cycles

- AI inferencing workloads (not training — inferencing)

- Nearline HDD supply gaps pushing high-capacity workloads onto QLC SSDs

The third driver is the new story. Training-side NAND demand has been on every analyst slide for two years. AI inference plus HDD displacement has been chronically underestimated.

HDD vendors have not meaningfully expanded capacity, QLC SSD density keeps climbing, and AI inference is latency-sensitive in a way nearline HDD never tried to serve. Once that loop closes, the NAND crunch is no longer cyclical — it is structural.

4. What this means for spot and EMS buyers

A few direct implications:

- Enterprise SSD spot prices, especially QLC 8TB and above, are not returning to 2024 lows this calendar year

- Small-capacity eMMC and industrial SSDs will get squeezed out of fab loading as QLC takes priority

- Long-lifecycle programs (medical, rail, energy storage, industrial controls) should ringfence NAND BOM pricing and add 6 months of safety stock

- Used, pull-from-system, and secondary-channel high-capacity enterprise SSDs — particularly 7.68TB and 15.36TB — will be hoovered up by server OEMs as allocation backstops, narrowing spread

5. Procurement playbook

- High-capacity QLC SSDs: lock 2026 H2 and 2027 H1 annual allocations directly with the OEM or tier-1 distributor. Do not gamble on spot

- Active POs: confirm date code, confirm fab line, plan for lead times stretching to 26 to 30 weeks

- Industrial and long-lifecycle programs: keep TLC where TLC still fits, reserve QLC for the workloads that actually need the density

- Secondary-channel sourcing: focus on 7.68TB and 15.36TB. These two SKUs will tighten first as allocation gaps open

- EMS customers on the nearline HDD side: their window to redesign 2026 H2 platforms around SSD is closing

6. Closing — this is not an inventory-rebuild cycle

Previous NAND price runs were mostly inventory cycles: destock to bottom, restock, price up. This one is different.

When Kioxia puts "sold out" on the table publicly, the message to every buyer is that structural demand plus capacity that cannot expand on cycle time is now the operating reality. Once AI inference and nearline displacement close the loop, QLC NAND in enterprise storage starts to look the way HBM looks in AI training: not a pricing problem, an availability problem.

For spot traders, the old "wait and prices fall" playbook is gone. Whoever holds allocation, holds inventory, and holds genuine OEM relationships in 2026 H2 is the one closing deals.