Published on: June 3, 2026

The Price Wave Just Moved From Memory to Power: Infineon's July 1 Second Hike and What Spot Buyers Should Do Now

Everyone spent H1 chasing DRAM, NAND, and HBM allocation. Power semiconductors got ignored. But Infineon's May 26 notice of a July 1 second hike, ST's full-line repricing, and Chinese MOSFET/IGBT makers raising 10-20% turn power into the second front of the 2026 pricing wave. Here's the breakdown for spot buyers: what moves first, where the window opens, how to source.

Lay the signals out first.

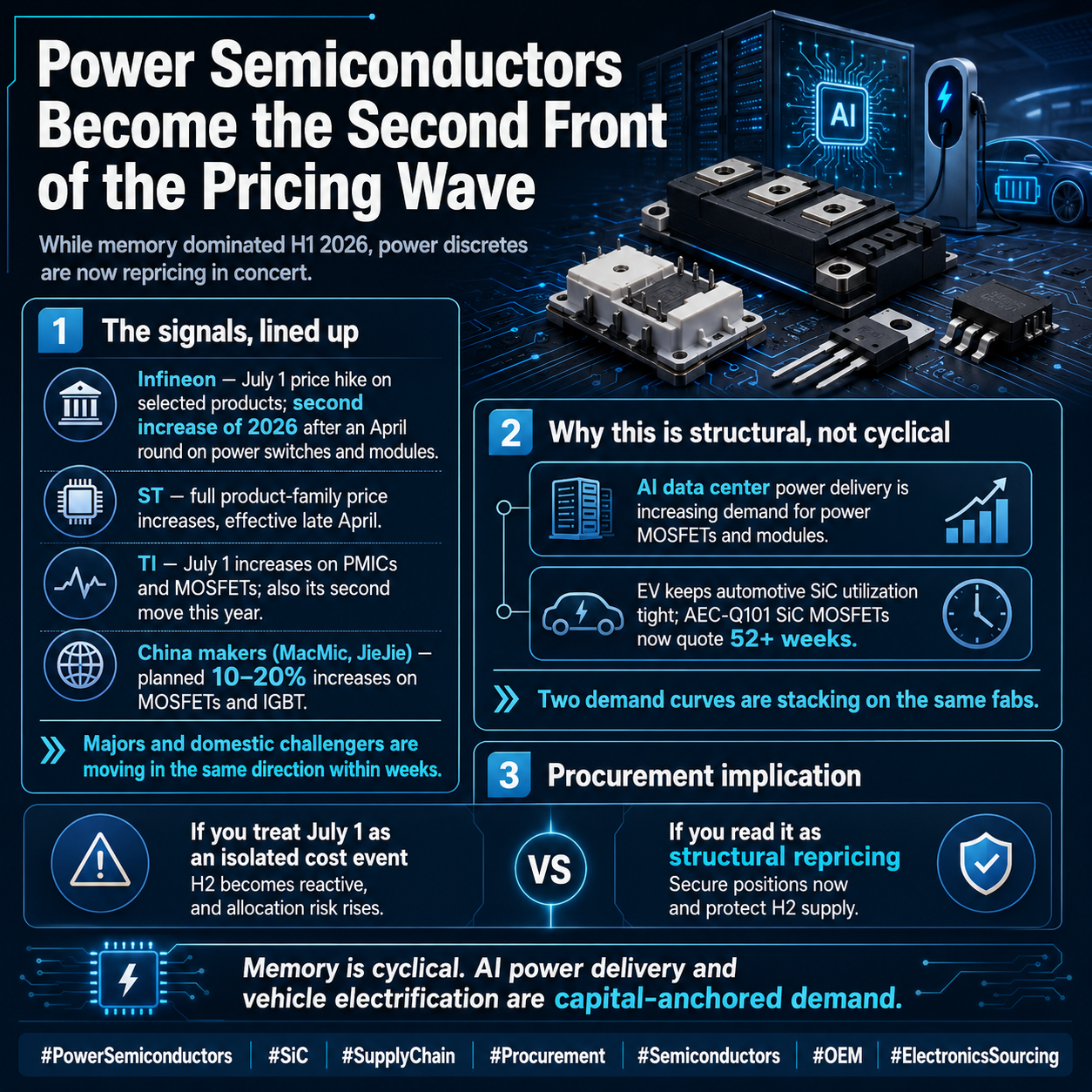

Infineon sent a customer notice on May 26: prices on selected products go up July 1. This is its second round of 2026 — the April round hit power switches, power modules, and related ICs with increases reported between 10% and 25%. The official reason is the usual stack: supply-chain costs, energy, raw materials, transportation all rising, while demand runs ahead of expectations.

ST moved earlier, notifying customers in March of increases across multiple product families, effective around April 26. TI lands on July 1 too, covering PMICs and MOSFETs — also its second 2026 hike.

Chinese makers aren't sitting still. MacMic and Jiangsu JieJie Microelectronics are planning 10% to 20% increases on MOSFET and IGBT lines. Majors lead, domestic follows — this is a full pricing chain, not an isolated move.

Why power? Two demand curves are stacking. AI data center power delivery — server PSUs, rack distribution, that whole layer runs on power MOSFETs and power modules. And EV, where automotive SiC demand is pinned at the ceiling. Automotive-qualified SiC MOSFETs are now quoted at 52 weeks or longer across multiple channels. AEC-Q101 SiC is the single most constrained category in the power market: limited wafer supply, long qualification cycles, and EV demand that won't quit.

For spot buyers, here's what to do now

One, re-screen your power inventory against the "will it land on the July 1 list" question. Tag Infineon power switches, power modules, gate drivers; ST MOSFETs and power ICs. Anything a customer orders after July is a spread sitting in your current stock.

Two, don't wait on automotive SiC. A 52-week lead time means the franchise channel is effectively dead for urgent demand. If an end customer has an AEC-Q101 SiC gap, spot and secondary channels are the only answer — and the quoting window is at its widest right now.

Three, the Chinese MOSFET/IGBT round is a clean match for dead stock. Domestic power parts sitting on your shelf have an exit window before the increase lands; after it lands, that same stock revalues up a notch on paper.

Four, watch PCN frequency. The denser the PCNs and the longer the lead times on mature part numbers, the closer obsolescence and shortage risk move. Power is likely to replay the memory rhythm: price first, allocation next, EOL last.

To put it plainly: power semis spent H1 in memory's shadow, but their fundamentals — AI power delivery plus EV — are more structural than memory's. Memory is a cycle; this power round looks more like a structural step-up. By the time everyone pivots to chasing power parts, the spot you can secure today is the leverage.