Published on: June 5, 2026

SLC and MLC NAND Just Became Endangered Parts: A Practical Sourcing Playbook for the Low-Density eMMC Squeeze

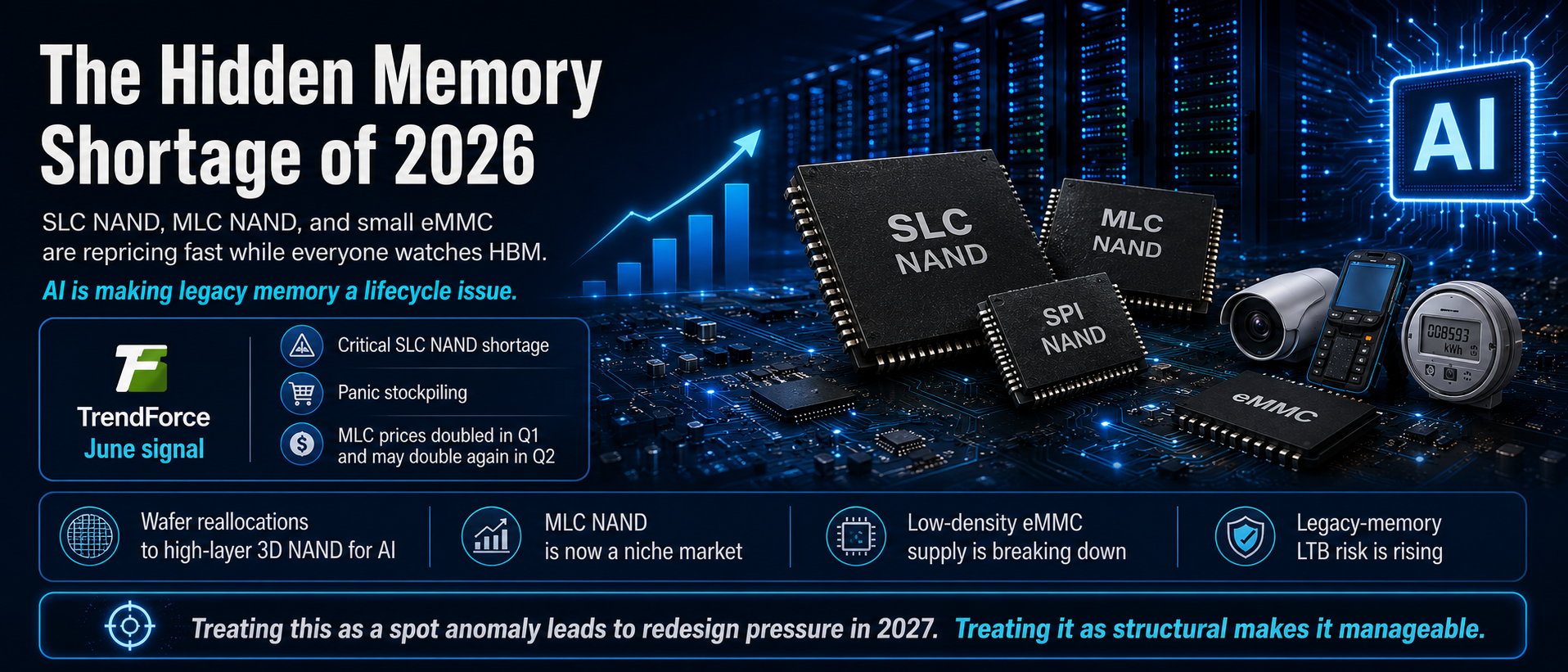

TrendForce's June data shows a critical SLC NAND shortage triggering panic stockpiling, while MLC contract prices doubled in Q1 2026 and may double again in Q2. The trigger: low-density eMMC supply disruptions as major fabs abandon legacy nodes for AI-grade 3D NAND. Here is a step-by-step playbook for industrial and automotive buyers.

What just happened

TrendForce's June update is blunt: a critical supply shortage of SLC NAND has sparked panic stockpiling and rare, dramatic price hikes. MLC inventories are depleted and still climbing.

The early warning came in March, when DigiTimes reported that low-capacity eMMC supply disruptions were dragging the whole legacy segment up — MLC contract prices doubled in Q1 2026 and could double again in Q2.

This is not the enterprise NAND story. QLC SSD allocation battles for AI data centers are one front. This is the other end of the spectrum: 4GB/8GB eMMC, SLC raw NAND, SPI NAND — the parts nobody watches.

Why this is structural, not cyclical

- Major manufacturers are reallocating wafer capacity to high-layer 3D NAND for AI servers and enterprise SSDs, cutting legacy nodes outright

- TrendForce called it in January: with the majors exiting, MLC NAND has officially become a niche market

- Meanwhile AI edge devices — smart cameras, gateways, AIoT endpoints — are pulling small-density storage demand up, not down

- Supply cut on one side, demand spike on the other, and no rebuild mechanism in sight

Who is picking up the slack

- Macronix: restarted NT$22B capex for MLC eMMC and NOR output, eMMC revenue up 94% QoQ and nearly 40x YoY — and switched to a monthly repricing model, which means quotes now expire in days

- Winbond: capacity fully booked through 2027, with lines also being shifted toward NOR

- GigaDevice: openly guiding that niche DRAM and NAND price increases will run through the end of 2026

Every niche supplier is running at full utilization. That is back-fill, not replacement — the volumes do not come close to covering what the majors abandoned.

Six moves for buyers, this week

- Audit the BOM: pull every SLC/MLC raw NAND, SPI NAND, and ≤8GB eMMC part number into a dedicated watchlist and raise its risk grade

- Push for LTB/PCN clarity: ask franchised distributors and manufacturer reps directly about unannounced discontinuation timelines — legacy-node LTB windows often come around exactly once

- Qualify alternates now: Macronix, Winbond, GigaDevice, Longsys/FORESEE, BIWIN equivalents should go into qualification before the line breaks, not after

- Shorten quote validity: your counterparties reprice monthly; quotes to your customers should not hold beyond 72 hours, with NCNR locked in writing

- Tighten incoming inspection: every sharp spot rally pulls refurbished, re-marked, and pulled parts into the channel — date codes, traceability, and visual inspection are non-negotiable

- Open the pSLC conversation: pSLC mode on 3D TLC is the credible long-term substitute for SLC in long-lifecycle designs — get your customer's engineering team onboard early

The takeaway

Phison's CEO says NAND prices doubled in six months and at least one foundry now demands three years of cash up front. If that is the treatment top-tier customers get, legacy parts will get worse.

AI did not just take HBM and DDR5 capacity. It took away the legacy nodes' reason to exist. Small-density parts are never watched — and in every discontinuation wave, the unwatched parts die first. Dormant SLC/MLC and low-density eMMC inventory may be the most underpriced stock of 2026.