Published on: May 20, 2026

DRAM and NAND Shortage Is the Worst in 15 Years — Three Things Procurement Should Be Clear On

The Q2 2026 memory shortage is the worst since 2011. HBM is pulling capacity away from consumer DRAM and NAND, and both price and lead time have moved together. Three practical takeaways for procurement.

The memory market looks different this quarter than it did last quarter.

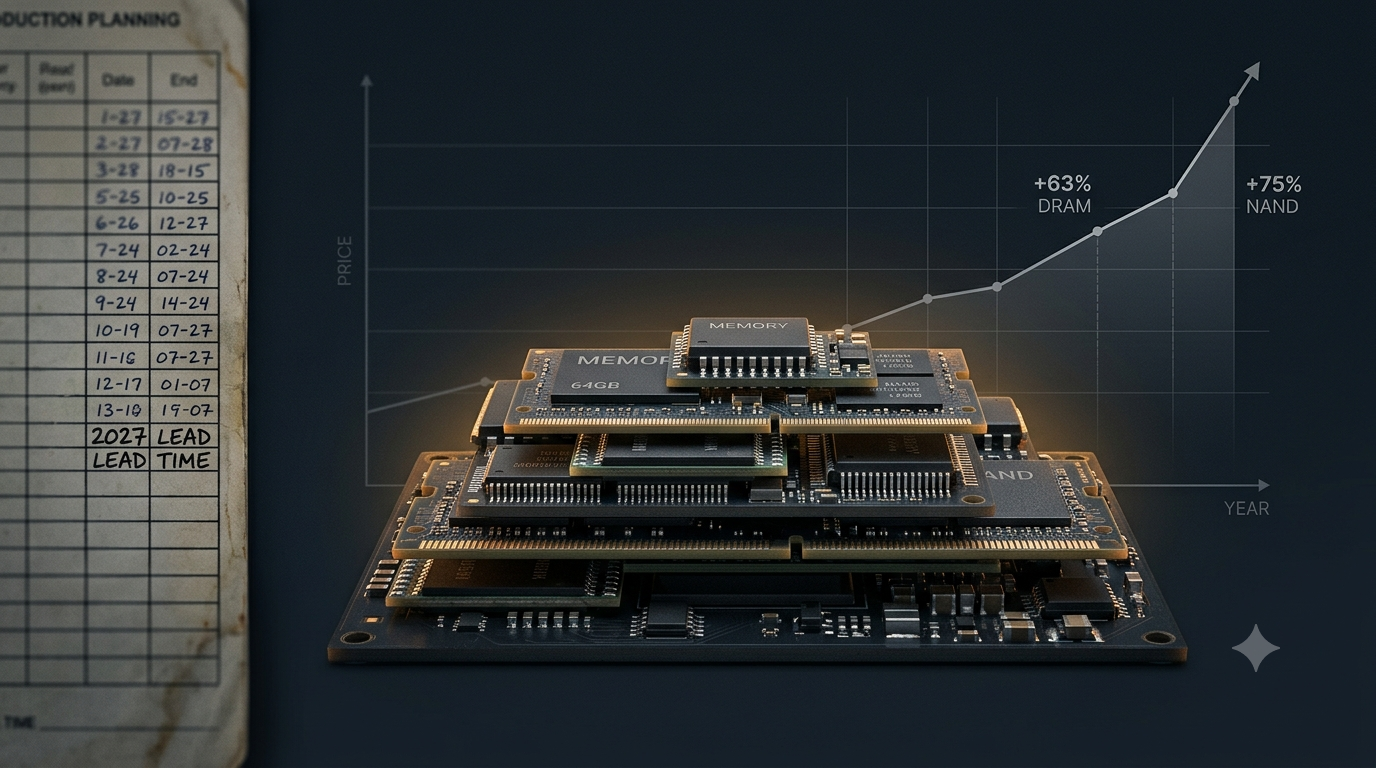

DRAM contract prices rose 58–63% quarter on quarter. NAND Flash rose 70–75%. Those are the largest single-quarter moves in a decade. Lead times have stretched past 55 weeks.

The cause isn't a single fab outage. Samsung, SK Hynix and Micron are all shifting consumer-grade DRAM and NAND wafers toward HBM to feed AI data-center demand. Everyone is doing it at the same time.

IDC puts the supply gap at DRAM 4.9%, NAND 4.2% and HBM 5.1% — all the widest since 2011. Goldman Sachs expects the imbalance to run into 2027. Lenovo has publicly disclosed inventory builds to protect 2026 production. Tesla has flagged DRAM availability as a vehicle-production risk. Smartphone shipments are projected down 12.9% and PCs down 11.3% for the year.

For end-customer factories, EMS providers and solution houses, this isn't a sentiment story anymore. It's a calendar problem. Three things to be clear on.

1. A 55-week lead time isn't a scary number — it's a date

If you need material in Q3 2027, you order today. Put the 55 weeks on a calendar: an order placed now lands after June 2027. If a BOM has DRAM, NAND or modules built around them, work back from the required delivery date and decide whether to order, how much, and when. Reacting after the production schedule slips is reacting too late.

2. Small-volume orders are getting deprioritized

Tier-1 distributors are choosing. Hyperscalers and long-term-contract accounts come first; sub-1,000-piece ad-hoc orders get pushed to the next allocation cycle, or refused. This isn't a short-lived squeeze — it lasts through the shortage cycle.

If your volumes have consistently sat near the bottom of a distributor's customer list, the only reason past orders cleared was that capacity was loose. Capacity isn't loose anymore.

3. Second-tier sourcing moves from "nice to have" to "needed"

This is the structural shift that's easiest to underestimate.

When tier-1 channels start turning away small orders or deprioritizing them, second-tier channels — excess inventory brokers, cross-border sourcing, obsolete and hard-to-find networks, OEM residual stock — stop being a cost-saving option and become a production-protecting one. The catch is that these channels are fragmented, information is thin, and quality varies. Finding a couple of vendors on short notice usually isn't enough; this is a capability that has to be built deliberately.

Q2 2026 isn't the quarter the shortage gets resolved. It's the quarter procurement structures actually get stress-tested. Teams that already have a working second-tier sourcing path will keep their lines moving. Teams that don't will spend the next year-plus building one under pressure.